Auto sales on the swiss market increased by 2.9% in 2012 and nearly beat the 1989 record level.

These results are remarkable in the continental economic context. After an analysis of macroscopic trends, let us have a look at models and segments.

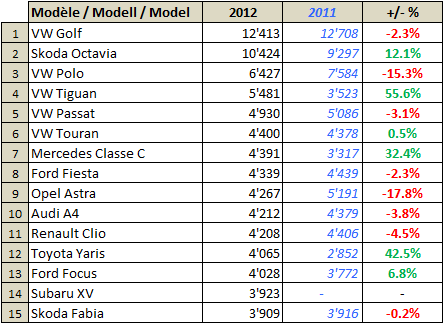

In the top 15 chart of the most successful models, no change in the winning Golf-Octavia-Polo trio, their volumes are out of reach for competition. Behind, several changes in the ranking, starting with the Volkswagen Tiguan whose facelift sent sales upward by 55% !

If the sligth softness of Golf sales can be associated with the transition to the seventh generation, the erosion of Polo sales is to place back in the context of outstanding 2011 figures. The Mercedes C-class was a very strong performer, beating the Audi A4 range thanks to an aggressive commercial strategy. The new Toyota Yaris is steaming ahead, returning to historical volumes of the 2006-2007 years. However, the biggest surprise of this top 15 is the Subaru XV: a good product at the right price in a trendy segment, which unseats last year’s leader, the Ford Kuga, in its first year of sales.

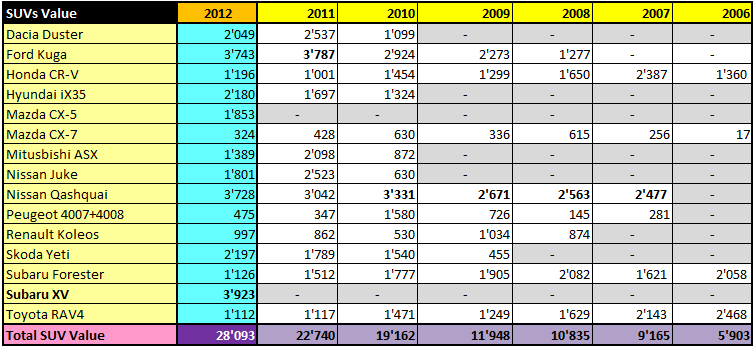

SUVs: +76%

Diesel and 4×4 are dominant trends on the swiss market, and if 4×4 & SUVs are not always synonimous, the growth of off-roadish models is meteoric, whichever subsegment you look at. In the value segment, the XV-Kuga-Qashquai trio dominates the market, leaving competition measurably behind.

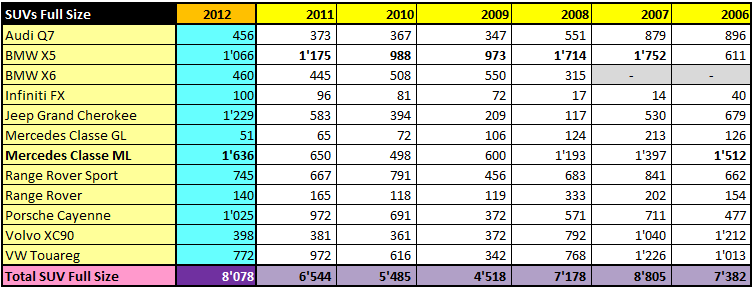

While affordable SUVs account for a large chunk of unit sales, sales amounts remain very attractive in the upper segments. Our analysis indicate that the Compact, Midsize and Fullsize segments generate as much turnover (and probably even better margins) than the more widely distributed models. The VW Tiguan is a star, not only through its growth since the facelift, but also in being the number one SUV model on the entire swiss market, all segments combined. The Audi Q3 had a successful launch, beating the BMW X1 and Range Rover Evoque. One size up, the BMW X3 has a solid lead. Among the behemoths, the new Mercedes ML emerges as the winner. Everywhere, the assessment is the same. Sales are growing briskly, the offering is widening. In comparison with 2011, combined unit sales across these 4 sub-segments have grown by 76% !

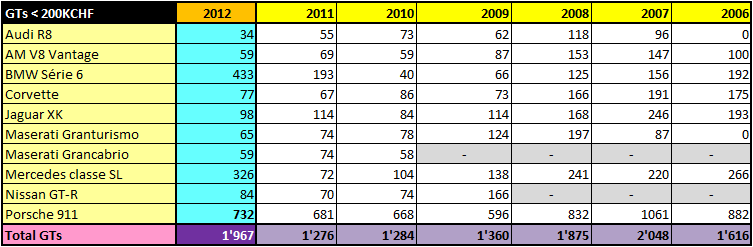

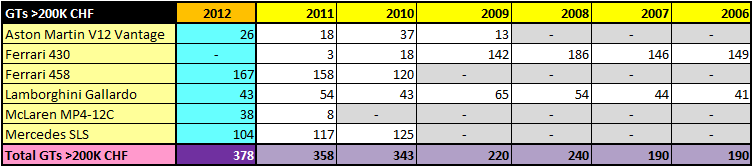

GTs: stable trend

At first glance, sales of GTs below 200’000 CHF are doing well, reclaiming ground lost during the subprime crisis. Closer scrutiny however shows that this is attributable to the launch of the new BMW 6 series and Mercedes SL. The other pillars of the segment are doing alright, but well below their pre-crisis levels. Even the new Porsche 911 is not enjoying the success one would have expected with the availability of the coupe, cabrio and more recently 4 & 4S versions.

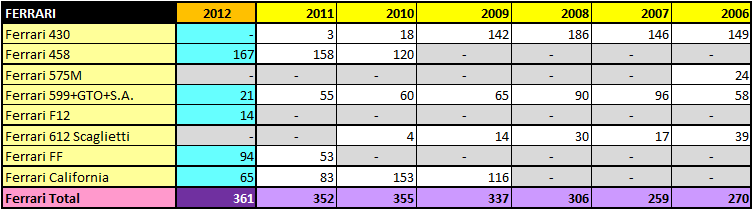

Same conclusion one class up on the pricing scale, GT berlinettas maintain robust volumes in the european context, but sales of the Ferrari 458 et 458 Spider have not reached the records hit by the 430 in 2008. The Mercedes SLS AMG continues to seduce swiss buyers, while deliveries of the McLaren MP4-12C are happening slowly. The Lamborghini Gallardo demonstrates amazing sustained resilience through a littany of special editions and refreshes, the most recent was presented at the 2012 Paris autoshow.

Same conclusion among the larger coupes in the same price bracket.

Ferrari sales are only growing marginally in their biggest per capita market, and this thanks to the extraordinary success of the FF. Sales of the Lamborghini Aventador are equally remarkable for a supercar whose base price is a breathtaking 433’000 CHF. No less than 6 Bugatti Veyron were newly registered in 2012, but ‘only’ 10 Rolls Royce Ghost (370’000 CHF), 9 Bentley Mulsanne (412’000 CHF) and 7 Rolls Royce Phantom (dès 580’000 CHF).

Overall, Porsche sales are good, but we were expecting better out of a great 911 model year. The strength of the Cayenne and the sustained success of the Panamera are not to be missed.

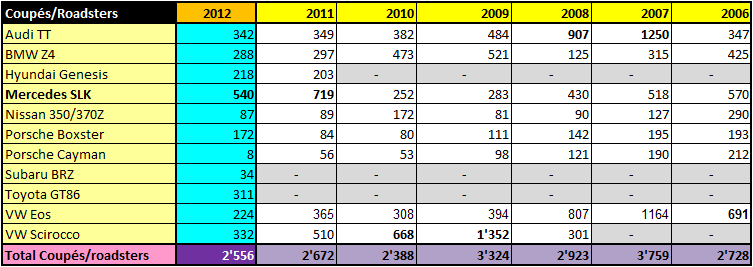

The market for more affordable coupes and roadsters is lukewarm. The hype surrounding the launch of the Toyota GT86 did not quite translate in success in the showrooms, and what can we say about the Subaru BRZ sister model ?

Look toward the US sports cars for stronger market dynamics, in particular the Chevrolet Camaro.

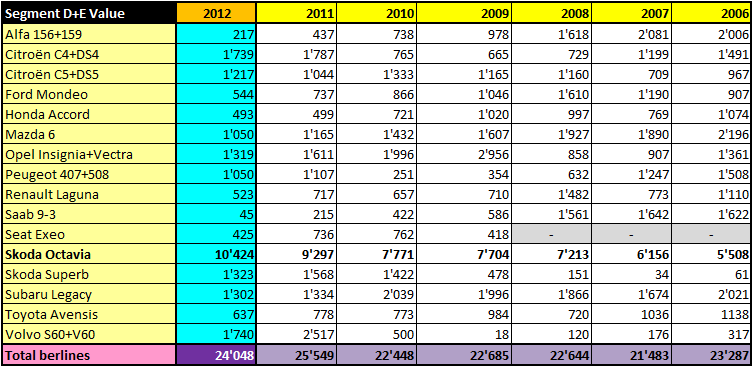

Sedans

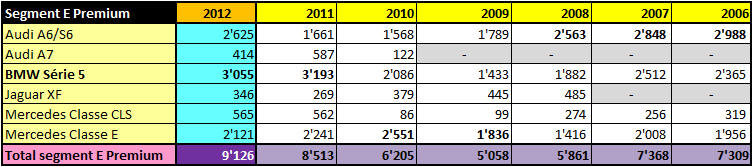

The D Premium segment should suffer from SUV cannibalization, but it actually grew by 6%, versus 2.9% for the whole market. Same results in the E Premium segment, which grew by 7%. A bit of softness can be found in the less prestigious D & E offering where far behjind the Skoda Octavia ogre, sales are overall declining by 6%.

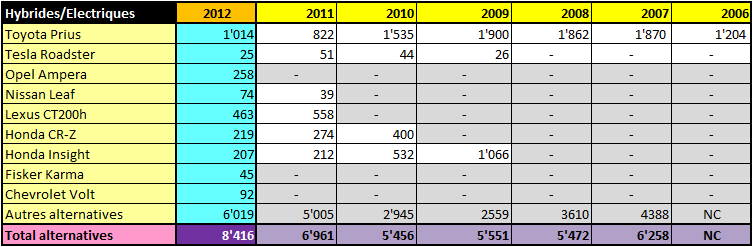

Hybrids & Electric cars

The share of alternative/hybrid cars is increasing, but more so through the sales of hybrid versions of mainstream models than dedicated models such as the Prius. New models such as the Ampera & Leaf are not making a breakthrough. Sales of the Fisker Karma seem to be running out of steam after the first wave of early adopters, monthly registrations sank from 14 in April and May to 4 from June through August, then only 1 to 2 cars per month since September. This does not quite look like momentum. It will be interesting to see whether the Tesla Model S does better in 2013.

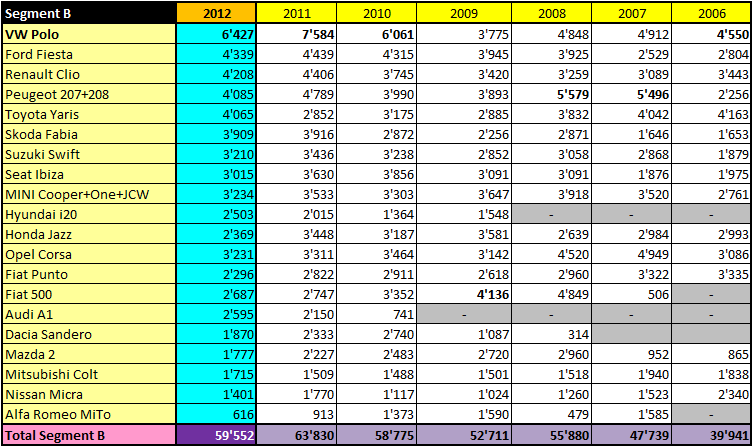

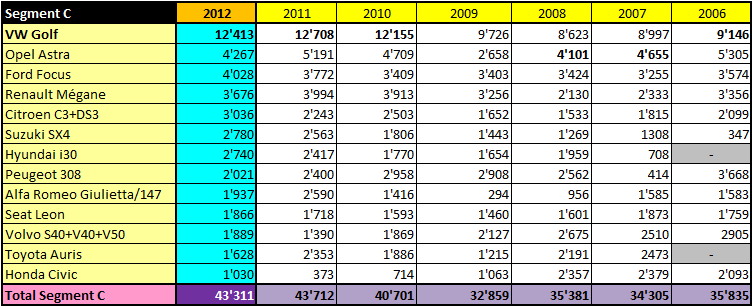

Compacts

Compact cars in the B & C segment are under pressure. Easy to notice, harder to diagnose. Media and economic context ? Migration of customers toward SUVs ? Backlash from an excellent 2011 year and replacement purchases anticipated because of euro-bonuses ? These segments represent a third of total volume, and growth is clearly not coming from them.

Liens

Le sujet du forum – les articles sur le marché suisse – les essais récents:

")