The swiss auto market shrank by 4.1% in the first semester 2014.

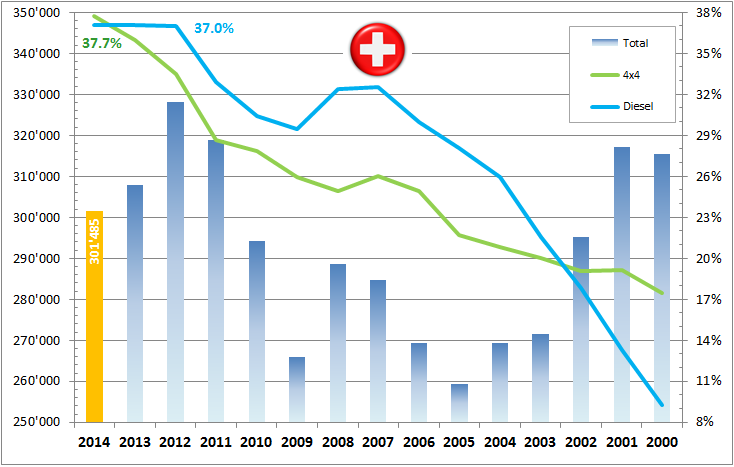

On a rolling basis over the latest 12 months, the swiss passenger car market remains above the 300’000 symbolic mark, but in comparison with the 2012 peak (328’139 units), the erosion in new car sales is significant. This comes in the context of a market that thrived during the euro crisis while other neighbouring economies tanked. Diesel share has been stable for 30 months at 37%, while sales of 4×4 continue to climb, reaching 37.7% over the past twelve months.

Brands: winners and loosers

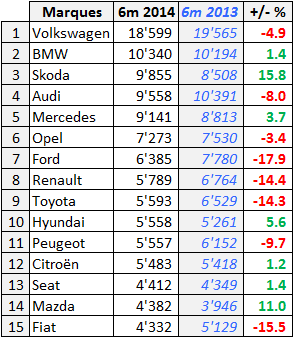

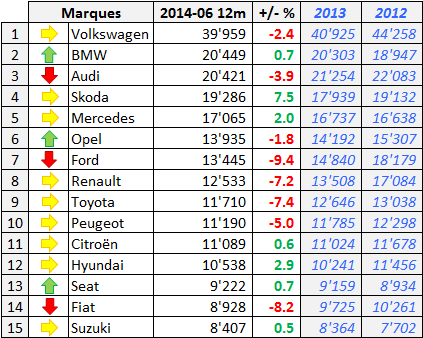

Volkswagen, the undisputed leader of the swiss auto market, has seen its sales decline faster than the overall market, a result that can almost entirely be attributed to the Passat whose replacement has just been announced early July. The outstanding performance of Skoda (+15.8% in the first semester 2014) goes to the credit of the Octavia and the Rapid. Audi has begun to stabilize its sales after a mediocre first quarter (-17.2%), but BMW retains a comfortable lead and its is difficult to envision a scenario where the 4 ringed brand retains its number one status in the premium segment. Mercedes grows by 3.7% in an overall declining market, a sign that its renewed and rejuvinated portfolio is paying dividends.

Among generalists, Ford, Renault and Toyota all record stark declines, same for Peugeot and Fiat.

Top 15 by model

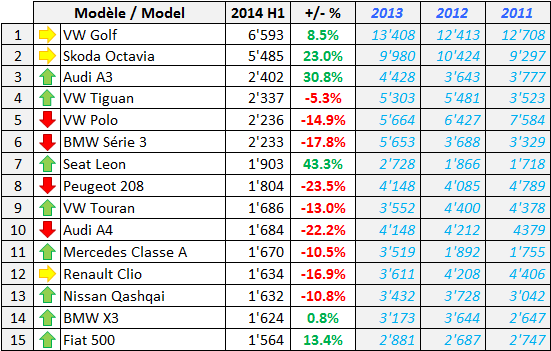

In the ranking by model, the VW Golf VII is selling well and remains comfortably in the lead, but it is really the new Skoda Octavia and Audi A3 which stand out. The new Seat Leon with its new sharper styling also seems to resonnate with customers. The breadth of offering contributes to fragment the market: 52 models sold 1000 units or more in this semester.

Hyperluxury ? Very well, thank you !

No less than 24 hypercars were registered new in Switzerland over the first six months of this fastuous era for superlative sports cars. Knowing that each retails for one million swiss francs or more, the figure is remarkable. Ferrari LaFerrari deliveries have outpaced McLaren P1, and it will be fascinated to watch which model stands out at the end of the year as the king of supercars in a market that draws a disproportionate share of this segment.

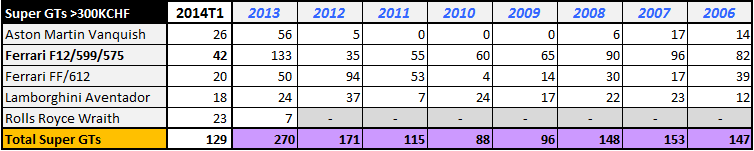

Super GTs continue to sell very well, even if one can’t expect that the Ferrari F12 will match its stunning sales figures from 2013.

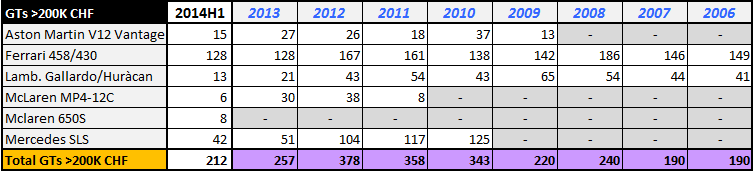

Ferrari mid-rear engine berlinettas are selling very well also, 458 matching its 2013 full year sales at the half year mark ! It is too early to gauge the appeal of the new Lamborghini Huracan with Swiss customers, but one cannot help wondering why the McLaren 12C and 650S figures look so pale.

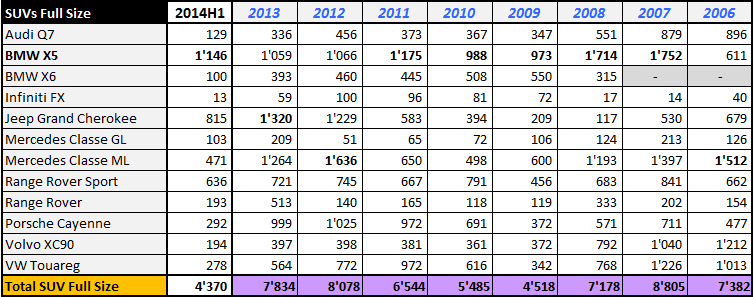

SUVs: Macan ?

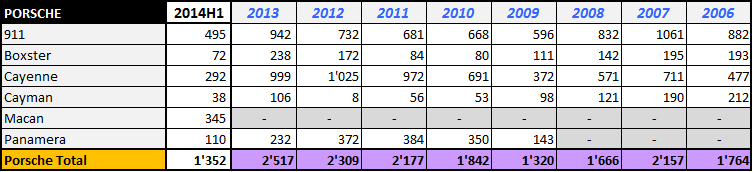

Deliveries of the new Porsche Macan started in the second quarter and appear promising. They are surely good news for the Porsche dealer network who other otherwise would have seen a 23.5% decline year-on-year. Sales of the new Boxster et Cayman, updated in 2013, have fallen back to confidential levels. Weak sales of the Porsche Cayenne raise the hypothesis of a cannibalization from the smaller Macan.

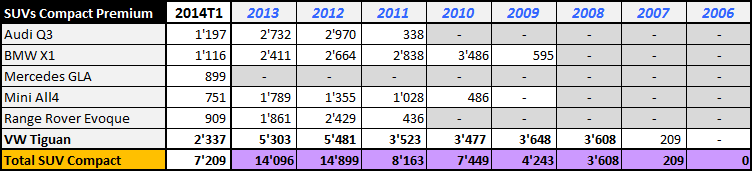

Sales of full size SUVs show good health, with an excellent reception given to the new BMW X5 and the Range Rover Sport. Among compact premium SUVs, GLA sales are boosting the segment, but it is too early to tell whether the Mercedes crossover will become a real challenger ot the X1 and Q3.

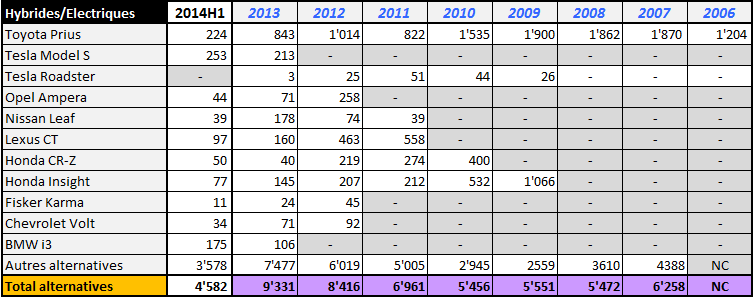

Electrics running flat ?

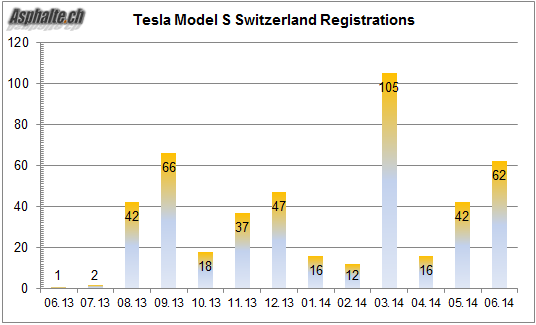

Tesla Model S sales continue, but do not seem to really take off. Two hypothesis can be articulated. The first is that the allocation of limited production capacity at the Tesla factory in Fremont, California is throttling the growth in the existing markets. The second would be related to true demand. With 253 cars sold in this semester, the Model S matches another niche luxury sedan, the Mercedes CLS, achieving only one quarter of the sales of the segment leader, the BMW 5-series.

Sales figures for the array of dedicated hybrids and electric cars shows that growth is actually coming from “soft hybrids” – lightly modified variants of mainstream models – rather than hybrids or electrical cars with a more radical definition. None of the models listed hereunder has really had success on the swiss market, or at least lasting success when the case of the Toyota Prius is considered. Sales of innovative products such as the BMW i3 do not seem to take off either. Is the charing infrastructure too limited ? Is value for money questionable ? These questions appear pertinent.

With volumes tending toward a soft landing at 300’000 units, a stable 37% diesel share since nearly 3 years and robust SUV sales, has the swiss auto market reached a new equilibrium ? We will test this assumption in the second half of the year.

Links

Forum topic – articles on the swiss auto market – the list of tests – recent or related: