Will new 2020 CO2 targets be a major challenge ?

Original french version of this article

With the deployment of the “95 grams goal”, 2020 heralds a new era in CO2 emissions from passenger cars, with likely consequences on the price of cars, but also on the product offering of battery electric and plug-in hybrid vehicles. Independent from the EU, the swiss automotive market is a fascinating laboratory for the observation of these dynamics.

Background

Switzerland first introduced on July 1st 2012 prescriptions on CO2 emissions from new passenger cars. While not a member of the European Union, Switzerland aligned on the goal to curb CO2 fleet emissions down to 130 g/km by 2015. This measure also served as a work-around to the anti-SUV ballot initiative instigated by the Young Greens party. This initiative, launched in 2008, targeted to outlaw all cars weighing more than 2.2 tons or with emissions exceeding 250 g/km. Political realities ended up prevailing over ideology, the swiss Parliament approved the 2011 Federal Act on the Reduction of CO2 Emissions, and the Young Greens withdrew their initiative.

In summary, this law requires:

1) payment of a penalty for exceeding a target CO2 emissions

2) computation of a CO2 fleet average for “large importers” (more than 50 new cars per year)

3) car by car payment for the small or individual importers of new cars

Implementation was staged:

1) staged phase-in: fleet emissions computed on the lowest emission part of the fleet: 65 % in 2012, 75% in 2013, 80% in 2014 then 100% in 2015.

2) increasing penalties over time.

The statute initially covered 2012 to 2018 and called for:

– 7.50 CHF per car for the first gram in excess,

– 22.50 CHF for the second,

– 37.50 CHF for the third and

– 142.50 CHF from the fourth gram above the target onward.

Article 13 however required that the Federal Council review the penalty schedule each year and shall base its decision on the amounts applied in the European Union and the exchange rate. The strength of the swiss franc against the euro resulted in CO2 sanctions being lowered several times.

For instance, the statute was revised on September 21st 2018 to:

– 2017: 5.50 CHF up to the first gram, 16.50 CHF for the second, 27.50 CHF for the third, then 104.50 CHF beyond, or 154 CHF for the first 4 grams of excess CO2 per km

– 2018: same but 103.50 CHF from the third gram

– 2019: 111 CHF flat per gram

The statute was again revised September 16th 2019:

– for 2020, the penalty is lowered to 109 CHF per gram in excess of the importer’s target

A honeymoon then the first warning shots

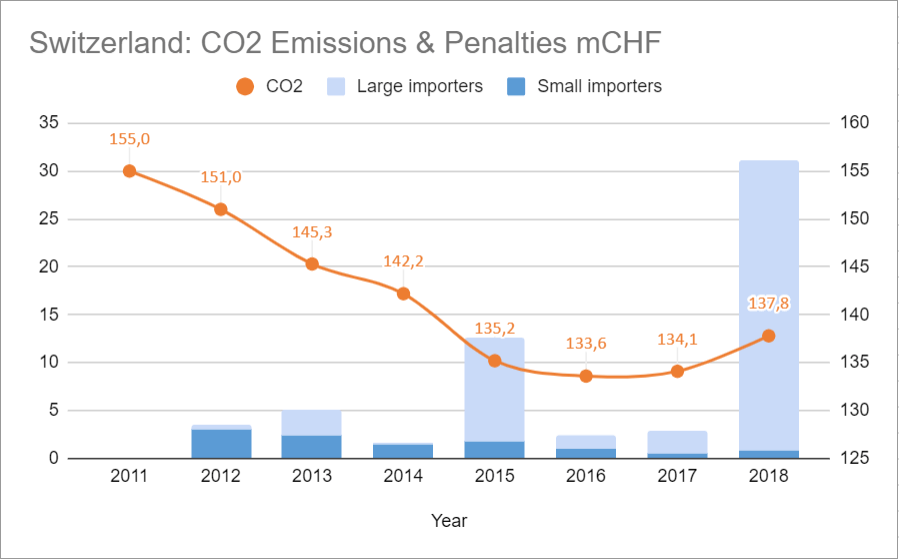

Initially, the deployment of CO2 targets appeared completely innocuous and mostly a tax deftly implemented by the automotive lobby in the swiss Parliament to curb direct imports. The strength of the swiss franc following the abandonment of the exchange rate floor policy by the swiss national bank. From 2012 to 2014, small importers pay 6.8m CHF of cumulated sanctions, large importers half that amount.

In 2015, the first warning shots are fired. Large importers pay 10.8 million francs in penalties. In 2016 and 2017, sanctions return to very low levels while the trend in CO2 emissions inverts itself. In 2018, CO2 penalties jump to 31.1m CHF.

Let us remind here that any company importing more than 50 cars per year qualifies as a large importer. In 2018, there were 77 such large importers, while only 25 can be considered as official. The largest parallel importers move nearly 2000 cars per year, but parallel imports represent only 4% of the swiss passenger car market.

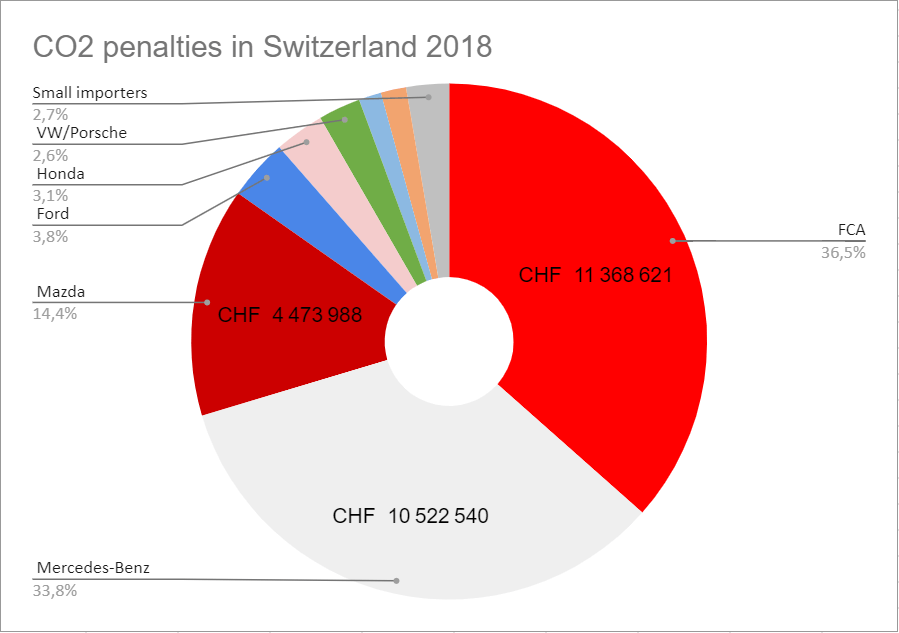

Fiat Chrysler (Alfa Romeo, Fiat, Jeep), Mercedes-Benz (& Smart) and Mazda pay the highest fines by far. To put these amounts in context, FCA or Maserati paid CHF 743 per imported vehiclefor 9.7g/km of excess above their respective targets, Mercedes CHF 494.5 for 7.3g/km of excess.

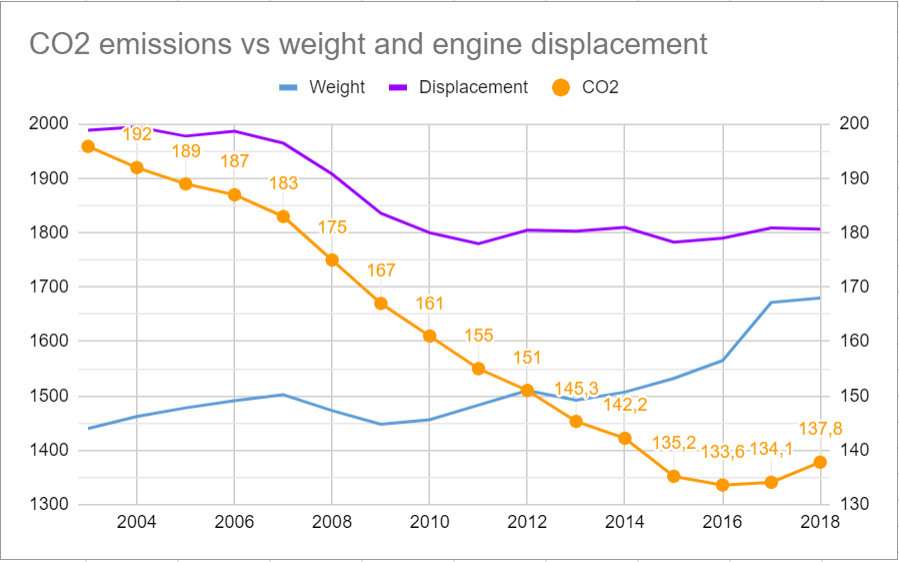

Where do these increases come from ? SUVs are often blamed, probably rightly so. The downward trend in displacement resulting from downsizing has plateaued since 2019 around 1800 cm3, nearly the highest in Europe. The weight of newly registered vehicles has increased by 12.6% from 2013 to 2018.

The sharp increase of four wheel drive vehicle sales on the swiss car market (share exceeds 50%) is also worth mentioning, but the confusion between 4×4 and SUV has become a trap. A significant share of sedans and compact cars have four wheel drive transmissions, so do most premium electric cars.

2020: the cliff ?

CO2 targets are dropping sharply in 2020. To simplify, the objective changes from 130g/km to 95 g/km. Actual targets for each importer (brands can pool their imports as they wish) depend on the average weight of the imported fleet. Small brands also benefit from waivers with specific decremental targets.

The 2020 targets are:

| Importer | Weight | 2018 | 2019 | 2020 |

| Alpina | 2172 | 218 | 216 | 214 |

| Aston Martin | 1897 | 297 | 295 | 290 |

| Bentley | 2552 | 286 | 264 | 245 |

| BMW & MINI | 1877 | 144,3 | 143,2 | 104,2 |

| Cadillac, Corvette, Camaro | 1907 | 267 | 265 | 245 |

| Peugeot, Citroën, DS | 1618 | 132,5 | 131,4 | 95,6 |

| Toyota, Lexus, Mitsubishi, Kia | 1691 | 134,1 | 134,7 | 98,0 |

| FCA | 1604 | 131,9 | 130,7 | 95,1 |

| Ferrari | 1746 | 289 | 286 | 280 |

| Ford | 1612 | 132,2 | 131,1 | 95,4 |

| Honda | 1372 | 121,3 | 120,1 | 87,4 |

| Hyundai | 1560 | 129,9 | 128,7 | 93,6 |

| Jaguar Land Rover | 1691 | NC | 178 | 130,5 |

| Lamborghini | 1949 | 315,0 | 304,0 | 106,6 |

| Lotus | 1199 | 225,0 | 225,0 | 225,0 |

| Maserati | 2258 | 239,0 | 237,0 | 235,0 |

| Mazda | 1503 | 129,4 | 126,1 | 91,7 |

| McLaren | 1549 | 265 | 260 | 250 |

| Mercedes | 1860 | 143,6 | 142,4 | 103,6 |

| Nissan | 1558 | 129,8 | 128,6 | 93,6 |

| Renault | 1421 | 123,5 | 122,4 | 89,0 |

| Ssangyong | 1859 | 167,6 | 167,6 | 103,6 |

| Subaru | 1609 | 164,6 | 164,6 | 120,7 |

| Suzuki | 1131 | 123,1 | 123,1 | 90,3 |

| Volvo | 1969 | 148,6 | 147,4 | 107,3 |

| VW, Seat, Skoda, Audi & Porsche | 1745 | 138,3 | 137,2 | 99,8 |

All importers in italic font met their 2018 goals.

As in 2012, the swiss government conceded to the automotive lobby smoothing measures to soften the blow.

| Share | Super-credits | |

| 2020 | 85% | 2.00 |

| 2021 | 90% | 1.67 |

| 2022 | 95% | 1.33 |

| 2023 | 100% | 1.00 |

Phase-in measures allow importers to ignore in the first three years a shrinking share of their highest polluting vehicles from the fleet emissions computation. The swiss phase-in scheme is more complacent than its European equivalent, 95% in 2020 then 100% from 2021.

Super-credits are granted to vehicles emitting less than 50g/km i.e. battery-electric and hydrogen cars, as well as many plug-in hybrids. The supercredit schedule is identical to the European Union. Counting lower or zero emission cars twice has a beneficial impact over the fleet average. There is a catch though: the contribution from super-credits cannot exceed 7.5 g/km in total over three years.

The miracle recipe ?

Are these new targets achievable and how ? How much do the phase-in and supercredits help ? While detailed mix information is hard to obtain, educated guesses can help understand the factors at play and size up the challenge.

Let us consider the case of the BMW Group which combines BMW, MINI and Rolls Royce. Fleet emissions were 140.7 g/km in 2018, under their 144.3 g/km target. The 2020 goal is 104.2 g/km. The BMW portfolio includes on electric vehicle, the i3, soon two with the launch of the electric MINI. BMW also has a growing number of plug-in hybrid variants (2 series, 3 series, 5 series, 7 series, X3, X5, and i8).

We start by dropping 15% of the volume with the highest emissions, or 4498 vehicles. For reference, BMW sold 3241 M cars in Switzerland in 2018. To reach 104.7 g/km, BMW would need to sell 25% of its 2, 3, 5, 7, X3, X5 in their plug-in hybrid variants to reach 104.7 g/km, based on the 2018 model mix. We assume here flat sales of the aging i3. However, the catch is that BMW then exceeds the super-credits cap by a lot, raking in 12.7 g/km in just one year.

In this scenario, BMW could not get below 110.2 g/km, translating into an average penalty of CHF 655 per car sold in 2020. Things then get worse in 2021 with 5% more high emission cars and zero contribution from super-credits.

Sticking with our 25% share PHEV and 1063 i3 sold per year, the 2021 average would reach 120.1 g/km, or 1737 CHF per car sold. Even if we substitute 500 X3 with freshly launch electric iX3 SUVs, 2021 emissions only go down to 117.7 g/km, or 1474 CHF.

If we bet on a more reasonable share of hybrids in 2020 and limit them to 10% instead of 25%, our simulation would exhaust the super-credit cap at 120.3 g/km, or 1758 CHF in average per car sold, then balloon to 130.9 g/km and 2906 CHF in 2021 with 90% of vehicles counted in.

These scenarii assume that mix remains constant, that consumers do not abandon SUVs to return to sedans or wagons, and do not account either for further gains in efficiency in from internal combustion engines, such as the introduction of mild hybrid systems.

Mercedes: a long way from home

Let us now look at another example, the Mercedes Group. Unlike BMW, Mercedes did not hit its 2018 target, closing the year at 151 g/km or 7.3 g/km above its quota. The group’s 2020 target it 103.6 g/km. By substituting 600 EQC to GLCs and achieving 10% of A, B, C, E and GLE classes in with plug-in hybrid models, Mercedes runs out of supercredits at 125.2 g/km, or 2358 CHF in average per car sold in Switzerland.

If EQC is a hit with 1’000 units in 2020 and consumers flock to A250e, B250e and the plug-in hybrid diesel versions of C, E and GLE product lines, the average drops to 116.8 g/km, or 1435 CHF of penalty per car.

Above the target

Commercial strategies will determine the impact on price lists. The least likely hypothesis is that manufacturers absorb these penalties by trimming their margins while they have to invest heavily in electrification, and the profitability of electrified cars is lower.

It is more plausible that the 109 CHF/g CO2 penalty will be reflected in the pricing of high emission cars. This will put large groups at a significant disadvantage in comparison with a few niche players.

Actual demand from consumers for battery electric and plug-in hybrid cars remains unknown. Switzerland is an affluent market, but there are no federal incentives on the purchase of low emission cars. In the last 12 months rolling, the share of electric cars on the swiss market was only 3.6%. This could turn into a heavily promotional environment in the second half of 2020 depending on how the actual mix of different importers evolves.

One thing remains certain: if CO2 targets have been relatively easy to meet up to now, things are going to change drastically as we enter into a new decade, ripe for profound changes in the choices made by consumers for their personal mobility.

Links

Forum topic – articles on the swiss automotive market– further reading: