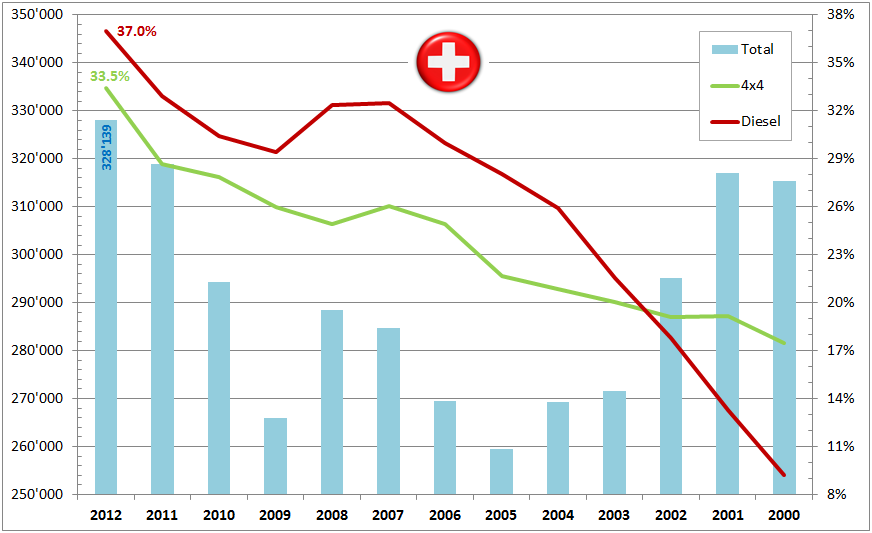

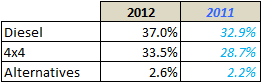

The swiss auto market closed 2012 on a new benchmark: 328’139 passenger cars registered anew, a growth of 2.9% over an excellent 2011. The absolute record of 1989 with 335’094 registration is not far. Trends remain centered on the growth of diesel engines (37.0% vs. 32.9% of sales in 2011), all wheel drive cars (33.5% vs. 28.7% in 2011). The share of alternative powertrains is growing as well, but remains small in absolute terms (2.6%).

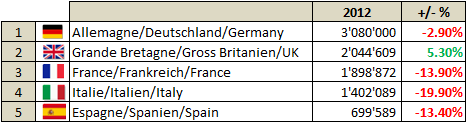

These figures are excellent on a comparison basis. All neighboring markets are eroding, if not collapsing. The only exception is the United Kingdom with a handsome +5.3%, but still 15% off 2007 levels, pre-subprime and pre-euro crisis.

Diesel and 4×4: the growth of these attributes seems relentless and has not reached a plateau yet. In the last quarter of 2012, the share of self-igniting engines reached 38.9%, and all-wheel-drive 36.1% of new registrations.

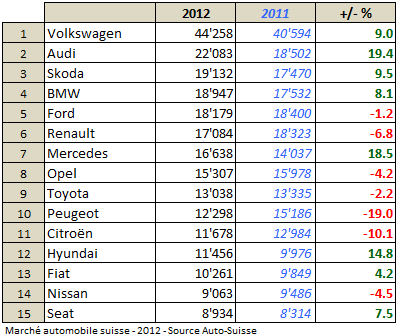

Little change at the top of the brand ranking. Volkswagen dominates the swiss market with a share double that of its follower, Audi. Sales of the premium brand in the AMAG portfolio literally exploded in 2012, with +19.4%. Skoda jumps from sixth to third while BMW maintains its second place within the premium brands, behind Audi but ahead of a strong Mercedes-Benz. Mainstream german and french brands are all suffering, in particular Peugeot. Note that Hyundai has more than doubled its sales volume in 3 years !

|

|

These figures are however to be balanced with the fact that the year ended with four consecutive months of contraction. It is possible that the new CO2 legislation played a role and pushed certain brands to accrue inventories through pre-registrations before the ax fell on July 1st. This incentive may have blown first semester figures to the detriment of second semester volumes. Auto-Suisse has released a prudent forecast of 295’000 units for 2013.

The forum topic – recent articles:

")