A revised study predicts a slow phase-out of the Internal Combustion Engine.

The Boston Consulting Group (BCG) has revised its automotive market electrification projections for the coming decade. The new study is a revision of projections first published late 2017.

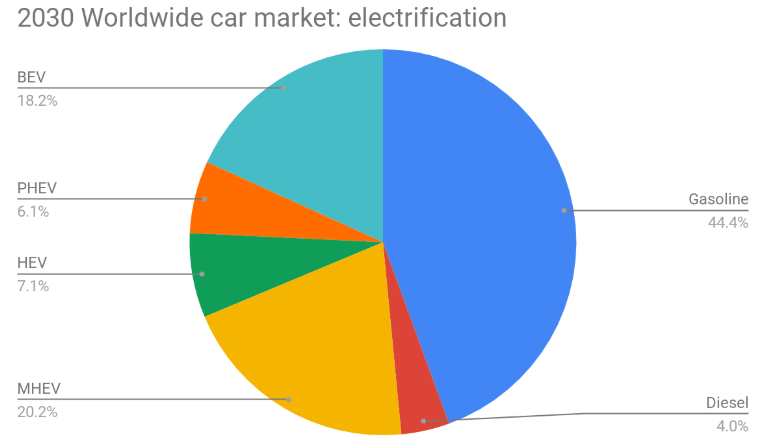

The main conclusion is that electrified cars will have a 51% share of the worldwide car market in 2030. The corollary is that 82% of new cars sold in 2030 will still have an internal combustion engine, assisted with different levels of electrification:

A reminder on acronyms:

– MHEV: Mild Hybrid Electric Vehicle, cars equipped with a low voltage hybrid system capable of recovering some of the kinetic energy to power components

– HEV: Hybrid Electric Vehicle, cars with a self rechargeable electric system capable of moving the vehicle in limited conditions

– PHEV: Plug In Hybrid Electric Vehicle, cars with a rechargeable electric system capable of moving the vehicle for short commutes

– BEV: Battery Electric Vehicle, purely electric car

According to the BCG model, electrification would not result in an industrial revolution and the mid term obsolescence of the Internal Combustion Engine (ICE), but in a gradual transition where an increased share of new cars sold integrate electrical subsystems: batteries, of course, but also motor/generators and power electronics.

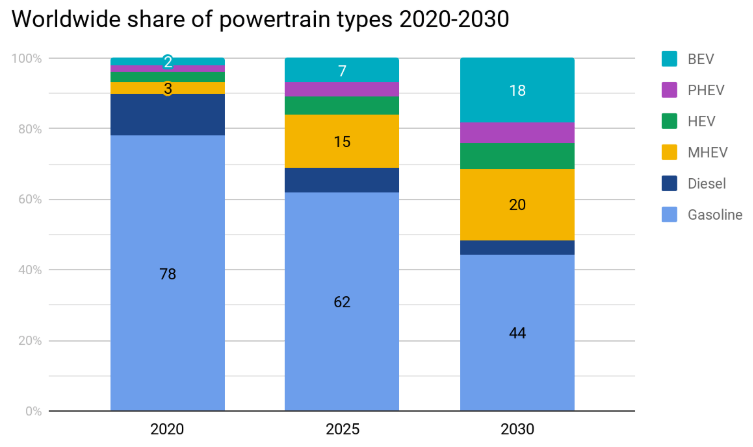

In fact, total ICE volumes would continue to increase to reach 100 million units in 2024, before slowly contracting to 90 million in 2030. Under these definitions, the growth of “xEVs” can be assimilated to astroturfing: cars get electrified, but remain widely reliant on fossil fuels.

Viewed at 5 year intervals, the transition is mainly driven by two factors: the adoption of electric cars by one fifth of the market, and the integration of mild hybrids by another fifth of the market.

Continents drifting ?

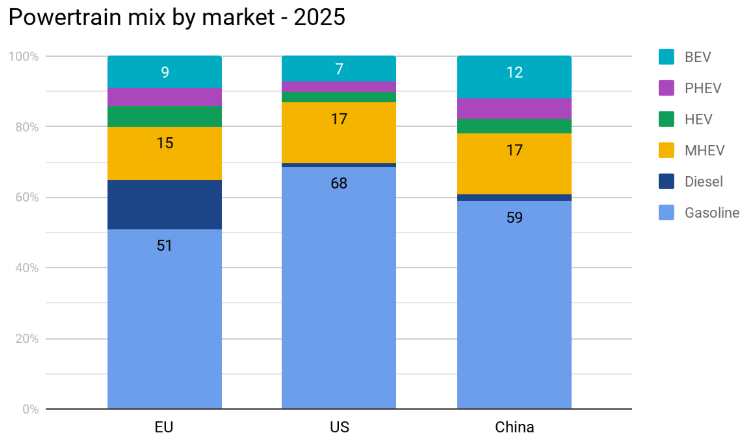

Are the three main auto markets, China, Europe and the US, drifting in different directions underneath these global numbers ? According to the BCG model, differences are expected, but they are not fundamental.

For instance, market share of BEVs is not expected to be significantly different in 2025 and 2030, in spite of contrasted government incentives.

| BEV Share | 2025 | 2030 |

| Europe | 9% | 25% |

| US | 7% | 21% |

| China | 12% | 26% |

The 2025 powertrain mix projection shows limited differences between regions, except for the diesel situation in Europe qui can be considered to be a variant of gasoline. Give or take a few percents, BCG projections are quite homogenous.

Working assumptions

What are these models built on ? The BCG study lists underlines a few interesting elements:

1) Short term, regulatory pressure in Europe and China accelerates electrification while the US lag behind

2) In the second half of the decade, total cost of ownership (TCO, purchase + energy) becomes a driving factor for adoption

3) Battery cost reductions is a key factor: BCG now forecasts 100$/kWh in 2030, versus 126$/kWh in their prior study, 2 years ago.

These last two points raise legitimate questions.

The revised BCG battery cost assumptions remain more conservative than other analysts, such as Bloomberg New Energy Finance who predict 89$/kWh in 2025 and 62$/kWh in 2030. The discrepancy is enormous and affects the most expensive component in an electric car.

Then, any TCO consideration has to be checked against fiscal aspects, and revenues derived from taxes on fossil fuels. In Europe in particular, states finance transport infrastructure by levying taxes on energy. A transfer from the gas pump to the electric socket will inevitably require a refactoring of the tax structure on the use of automobiles. An increasingly electrified fleet (with an increasing weight) will have to generate the same tax revenues as today’s largely combustion fleet, thereby eating into a TCO advantage largely based on untaxed energy (electricity from the grid).

Mobility pricing is seen as the only way to address chronic congestion at peak hours. To have the expected effect on road congestion, different powertrains will have to be treated in equivalent ways.

Finally, one would expect that large scale deployment of renewable electricity production sources, and the associated large scale energy storage infrastructure, will have a detrimental impact on electricity prices. Nuclear and coal/natural gas production are widespread incumbents because they provide a cheaper supply bedrock.

What about battery supply ?

If one assumes BEVs at a 50 kWh average, PHEVs at 15 kWh, HEVs at 1.5 kWh and MHEV at 0.5 kWh, BCG projections translate into a worldwide demand of 459 GWh in Lithium Ion cells for 2025.

SNE Research projects total installed Lithium Ion production capacity at 2025 à 1000 GWh. Cell production capacity should therefore not be a bottleneck.

Supply of raw materials, such as lithium, nickel, cobalt or copper, is more complex to analyze, furthermore as cell chemistry can vary between cell suppliers and, sometimes, car makers.

What about CO2 sanctions ?

Are BCG projections compatible with the regulatory constraints imposed on car manufacturers ? We will skip here New Energy Vehicles quotas imposed by China and whose formula is exceedingly complex.

In the European Union (and by extension in Switzerland), CO2 targets are 95 g/km in 2020, 81 g/km in 2025 and 59 g/km in 2030, adapted for each manufacturer group based on weight.

Our scenarii lead to the conclusion that BMW or Mercedes would have to sell in Europe significantly more than 10% of their volume as PHEV or BEV to avoid heavy yearly fines. The BCG study only projects 4% of BEVs and 4% PHEVs for 2022 for the whole european market.

At the leading edge of electrification of a traditional portfolio, VW Group, the world’s largest automaker, forecasts to reach 6% of european sales with BEVs in 2020 and 26% in 2025. Audi, the premium mass market brand of the group, targets 40% of its 2025 worldwide sales to come from electrified models (MHEV + PHEV + BEV).

BCG is explicit in its conclusion: without further incentives, automakers are going to miss their CO2 targets and pay substantial fines.

Eye on the ball

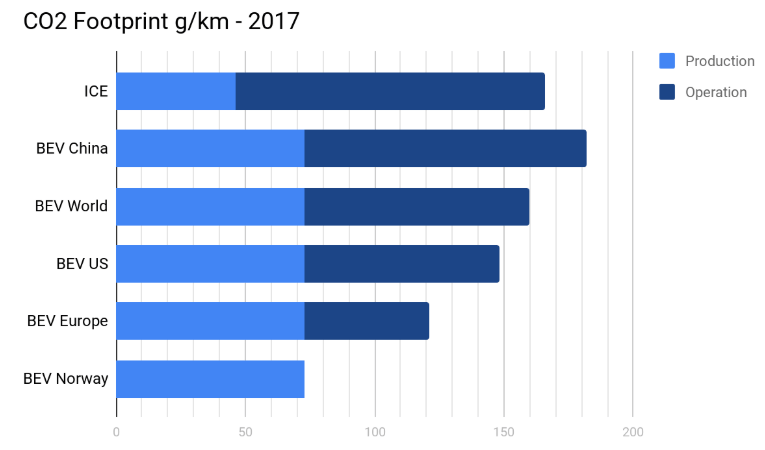

The BCG study includes in exhibit 5 a CO2 footprint analysis for variants of a C-segment compact car, driven over a life cycle of 150’000 km:

The pertinence of these assumptions and results depends in part on where the time marker is set: present time ? 2025 ? 2030 ? The overall conclusion remains however the same as in the other studies we have examined: in climate terms, electric cars are at worst equivalent to combustion cars with dirty electricity, and beneficial when the grid becomes cleaner.

Converting the car fleet to electric power is therefore a necessary condition for sustainable mobility, but not sufficient. Production and storage of clean electricity are mandatory to achieve the stated goals.

Links

Forum topic – car industry articles – further reading: